If you watched our last Q4 2023 Quarterly Update video, specifically where we discuss our Non-Performing Loan investments (“NPLs”), you probably heard us throwing around the term “securitization.”

Simply speaking, securitization is the process of pooling a group of mortgage assets together and repackaging them into more marketable securities. With these new asset-backed securities we are then able to create interest bearing bonds and can sell said bonds, consisting of a variety of different tranches, to institutional investors. These bonds are often referenced to as “Residential Mortgage-Backed Securities” or (RMBS for short).

At PPR, we use the securitization process to “refinance” our portfolio of NPLs, achieving several positive outcomes that further de-risk our overall investment portfolio by recapitalizing our mortgage holdings and lowering our cost of financing.

How it works

As it relates to the financing of our NPL investments, securitization is often our end goal. We start this process by aggregating our NPL acquisitions using Tier 1 short-term financing facilities and when our portfolio reaches a critical mass, which can vary depending on the market (for us, usually around $200M of the collective UPB or unpaid principal balance), we can then securitize our portfolio of loans to lock in longer term financing that is accretive to the portfolio. Refinancing by and through this process provides us with a fixed interest rate facility with no immediate “mark to market” margin call risk.

Additionally, securitizations provide us with a higher return (via an “advance rate”) to our portfolio’s market value than our short-term financing facilities. This higher advance rate also allows us to deleverage our equity capital position in the pool of assets and as such, further de-risk our collective investment and reinvest those proceeds into new assets.

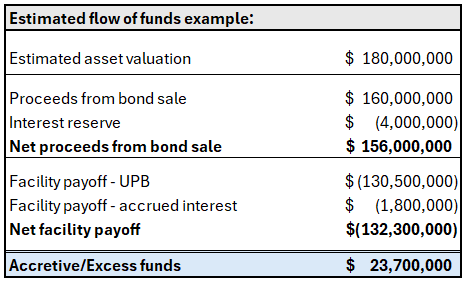

Below is an example of how we use proceeds from a securitization to pay off the short-term financing facility and unlock capital within our current investments faster than initially modeled:

*Note, the numbers in this example have been generalized for clarity

PPR and our Joint Venture partners’ Capital Markets team also saw significant activity in the RMBS marketplace towards the beginning of the new year. Initially our bonds were oversubscribed over 4 times the demand than we had supply. While past results are no guarantee of future success, the long-standing success and expertise of our NPL partners has allowed us to attract top quality bond buyers, which drives up demand while lowering the cost of the financing we pay on our investments. So with all that in mind, we’re excited about the 2024 NPL acquisitions and future securitization opportunities.

How we strategically approach the investment process and the support we achieve with our partners from bond buyers in securitization, allows us to deliver the optimal risk-adjusted returns on our collective NPL investment. Our strong execution on our securitization activities, successful bidding outcomes, increasing supply of assets, and a favorable economic backdrop for investing gives us the confidence to continue the aggregation cycle in 2024 and acquire the next wave of NPL trades.